Go to any of the dozens of conferences dedicated to the Internet of Things (IoT), and you’re likely to hear it: “The consumer IoT isn’t gaining adoption at the rate initially hoped.”

That matches with my anecdotal experience – at least amongst my non-tech friends, for whom being the first on the block with some new gadget doesn’t constitute a value proposition. One friend was even annoyed that her boyfriend bought her a Nest: “I just want a stupid thermostat!” But, being anecdotal, my experience doesn’t really tell us anything about what’s going on in the wider context. So I set about to see if there was any data to quantify what’s happening with the Consumer IoT (CIoT).

Luckily, I didn’t have to look back further than last August to find several surveys that had been done to quantify where we stand with the CIoT. These are surveys by:

- ISACA (formerly Information Systems Audit and Control Association); IT-oriented, with a focus on security;

- Accenture, a business consulting firm;

- Coldwell Banker, in association with CNET, with a distinct real-estate angle; and

- IDC, an industry analysis firm, via a webcast.

I also spoke with John Feland of Argus Insights. Unlike the other data sources, Argus looks at internet artifacts – discussions on social media, sentiment, benefits, problems, etc. – to gauge where things are headed. Also unlike the other sources, they don’t get absolute data in terms of market penetration. They gauge momentum and change – I refer to them as measuring the 1st derivative of the absolute data, but not the absolute data itself.

I’ll link to published reports below so that you can see or further analyze their methodologies.

Defining the CIoT

The first thing I learned when going through these different sources is that they’re not all measuring the same things. I probed for more detail, especially with the surveys that gave results I found surprising, and so I got some of the definitions they used. And, to some extent, how you define this area of technology depends on whether you focus on “Internet of Things” or “Smart Home” as a defining characteristic. “Connected devices” never came up as the name of a category, although it accurately describes the most common so-called “IoT” or “Smart Home” items, as we’ll see.

For example, Coldwell Banker’s definition was, “by ‘smart home technology/products’ we mean products or tools that aid in controlling a home’s functions such as lighting, temperature, security, safety, and entertainment, either remotely by a phone, tablet, [or] computer, or with a separate automatic system within the home itself.” But IDC requires that devices be able to access the internet “bidirectionally and autonomously.” That leaves out wearables like Fitbits that pair to a phone, where the phone ties into the internet.

Argus, meanwhile, includes anything that Best Buy and Amazon call “smart home.” They also exclude wearables. Mr. Feland mentioned that he had seen definitions as broad as “anything with a radio,” but that adds phones and tablets and computers, messing up the works.

There’s even more nuance when you look at specific included devices. The ISACA survey, for instance, included a few things that I question. I was clued in by the fact that they report 34% of users having from 5 to 10 IoT devices in the home; I was having a hard time coming up with that many devices.

- Employee access cards: they may be IoT and they may happen to be in the home because you come home at night, but they’re not home IoT – they’re enterprise IoT.

- Cameras that upload to the internet. This certainly meets the direct-connection-to-the-internet standard, but if all it does is store photos, then there’s no real “smart” involved; it’s essentially a smartphone without the phone and the smarts (only the camera and an uplink connection).

- Cars with GPS. Seems to be stretching the definition really far. There’s no internet involved with GPS.

- Electronic toll collection devices. Again, another stretch. I doubt that consumers view this as an IoT thing (and they’ve been around for longer than the IoT has been a common buzzword).

- Smart meters: these exist not due to customer purchase or adoption, but because utilities unilaterally made the switch (to much protest in some areas). While such a device could be considered CIoT (albeit debatable), their prevalence therefore doesn’t say anything about consumer adoption.

- Even smart TVs: if what they do is move storage and channels to the internet, then there’s not much in the way of smartness. This is important because such entertainment devices make up a huge chunk of what some reports claim as CIoT adoption (e.g., 43% of the population have smart TVs according to ISACA).

As full disclosure, my own definition – which I’m suppressing for the moment – includes connection to the internet (perhaps by proxy through a phone), but where something useful goes on in the internet to provide control to the device or other devices. This tends to rule out situations where the only difference between an old-school device and its internet version is simply that you can use your phone as a remote control. Looked at another way, a “connected” device wouldn’t necessarily be an IoT device.

I even lump phones, uploading cameras (maybe), tablets, and watches together not as IoT, but as alternative computing platforms. I’ll toss out an acronym I made up to give it more validity: a CoSE (pronounced “cozy”), or Computer on Something Else.

For remote-control applications, the internet isn’t providing “smarts”; it’s providing only a connection to the phone. Not that those remote control functions aren’t useful; they’re just not smart. But, according to Coldwell Banker/CNET, 76% of respondents use a phone to control their devices, with 40% controlling more than one device. So this makes up a big part of what’s viewed as IoT adoption.

There were other results that made me cock an eyebrow. For example, 77% of Coldwell Banker/CNET respondents consider themselves early adopters (84% for ages 18-44). That pretty much doesn’t leave many people to be normal or late adopters. It reminds me of my own version of the 80/20 rule: 80% of the people view themselves as being in the top 20%.

So, while I’m not imposing my definition outright, I did use these anomalies to filter the results in an attempt to make more sense out of them.

Is there CIoT adoption?

So now that I’ve muddied up the data enough to draw pretty much any conclusion I want, let’s look at adoption rates – and then we’ll look at why those might be low (and, with suitable filtering, they are low).

Cutting to the chase: existing adoption of devices actually requiring some smarts tends to be in the 10% and below range. For instance, ISACA found that 10% of respondents had smart home alarm systems. From there, it decreases through toys, watches, weight scales, garage door openers, medical devices, door locks, and baby monitors, finally bottoming out with refrigerators – the poster appliance for the CIoT – at 1%. Accenture saw virtually no increase in intent-to-purchase over last year.

Argus is dividing the space into three categories: Fear, Fun, and Function. Fear is getting the most traction – which means home security devices and cameras – while Fun is proving to be less than fun due to ease-of-use issues. For instance, connected lightbulbs seem cool (oooooo, pretty colors – we can pretend we’re in a Virgin America cabin), so the hardware is ok. But the app – well, why simply flip a wall switch when instead you can locate your phone and, to quote Mr. Feland, “with 12 clicks” (or was it 7?) manage to control the lights?

While ISACA saw the share of people with plans to buy a new connected watch increased to 17% over the prior year, plans to buy a connected car decreased to 11%. And 40% of respondents plan to buy “none of the above [devices].” To be clear, we don’t know whether that’s because they want nothing or because they want something not on the list.

So, what’s wrong? Industrial IoT (IIoT) adoption is moving right along. I don’t have numbers, but there has been activity in that space since before it was called IoT (then it was just M2M). Something seems qualitatively different about the consumer space.

Coldwell Banker/CNET generally reports shiny happy existing users, although the report is written in a very bullish manner – it feels like they want the numbers to be high. They report that 57% of those who currently own devices save time (on average, 30 minutes a day), and 45% say they save money (on average, more than $1100 per year). Even though that leaves out a lot of people, they draw the conclusion that the IoT “saves Americans time and money.” Their results also show that 91% of those with IoT devices would recommend that others dive in.

But other sources point to ease-of-use issues with the current round of available devices. Accenture found that, of existing users, 18% couldn’t get the device to connect to the internet; 16% found the devices too hard to use; 14% had setup problems; and 13% didn’t feel like the devices, once up and working, performed as advertised. Not huge numbers individually, but if we assume no overlap between those groups (not unreasonable, roughly speaking), that adds up to 61% of purchasers being unhappy.

Installation is a big issue, with three categories: do-it-yourself, do it with someone holding your hand, or have someone else do it. In fact, home security systems have a long history of installation by someone else, and they’re finding traction as installers of choice beyond security, according to IDC, beating out utilities (who normally don’t install inside the home).

Argus described a phenomenon where a purchaser has a limited window of time before a device can be returned. Given that installation will be a project, they have a few weekends to get the job done – but support is spotty on weekends, meaning hours waiting on the phone. If it takes a long time, but eventually works, perhaps it’s ok. But if the process makes you change your mind about the purchase, then spending too much time trying to get it to work pushes you out of the return window.

Argus can discuss numerous anecdotes involving ease of use (which they acquire through social media). For instance, many apps assume a single user, which is a poor assumption for a home. Google had an issue where smoke detectors would shut off with a wave of the hand, and no one would realize. (Reminds me of another gesture fail from the past…)

Other issues for current users relate to the connection. While IDC mentioned that the IoT, including cameras, makes few demands on bandwidth, Argus counters that HD cameras can upload gigabytes of data, slowing down other internet functions. WiFi access can also be an issue, since many IoT devices might be installed in places where the WiFi signal isn’t strong (like security devices outside the home).

Is It Time to Join the Party?

So it’s a mixed bag for the early adopters. What about the people still standing on the sidelines? What’s keeping them back? Well, scary ease-of-use stories don’t necessarily help. Argus says that a number of Google Nest devices given as gifts are never installed. (So, apparently, my friend has company.)

But there are other issues as well. Security, of course, is a big one. While security-related applications are doing relatively well, the perceived lack of privacy and security on the internet is a barrier. Probably no surprise there.

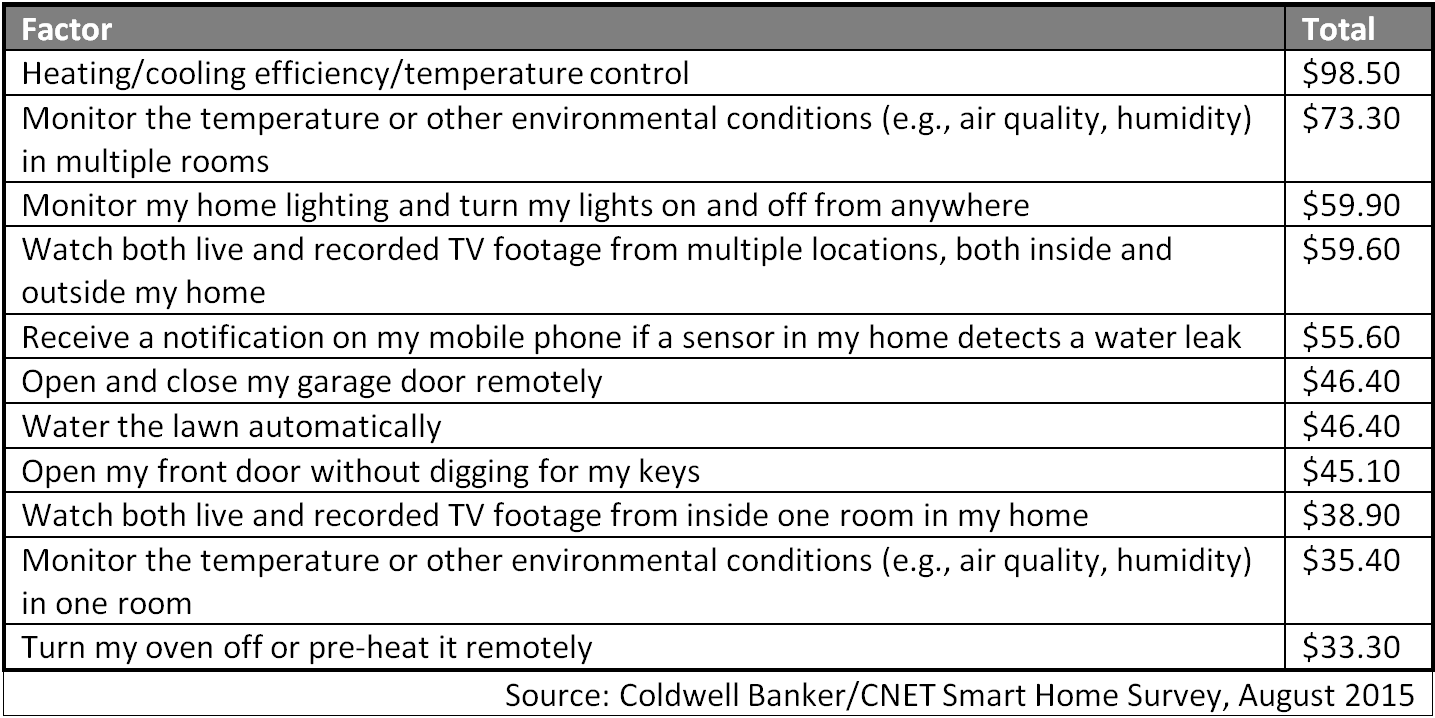

Pricing is also an issue. Accenture found that 62% – the largest chunk – found high prices to be a barrier to purchase. The Coldwell-Banker/CNET study asked what folks would pay for a range of devices. And they didn’t ask in ranges; it was an open-ended question, and the respondent could provide any answer they wanted. So they’re interesting data points (albeit without information on spread or deviation around the averages). I’ve adapted their table below for anyone trying to price their devices.

Average Dollars One Would Be Willing to Spend for Specific Smart-Home Items

(Among those with Smart-Home Products in the Home)

But this pricing gets to what seems to be the biggest (or, at least, the most consistent) source of malaise: lack of a clear perceived value proposition. Honestly, thinking about Coldwell-Banker/CNET’s result on time and money savings, I can’t think of smart-home devices that would save me 30 minutes a day or $1100 per year, but maybe that speaks to my lifestyle rather than any general truth.

I tried delving into this topic a while back in some detail, running through a fictitious smart-laundry-appliance example to see where the value might be. That discussion focused to some extent on monthly service fees, since the ideal future model (for providers) is a service model, not a device model. But whether it’s hardware or service, it’s money out and, cool factor aside, it should provide a benefit or a return on the investment.

One lesson that became all too clear to me back in some painful marketing days is that it’s not enough for people to say they’re interested in buying some thing. Talk is cheap, and there’s lots of talk. And people generally like to be nice and say nice things (which don’t pay the bills). Some surveys show large pools of people with intent to buy. But if they’re really going to buy something, it means they’ve got to:

- Get off their butts.

- Figure out what item(s) they want to buy.

- Figure out what works with what. (That takes research.)

- Select a brand. (That also takes research.)

- If they’re not so confused that they give up at this point, then they need to shell out some money.

- Then there’s installation.

- Then there’s consistent use ongoing (a month or two of novelty use doesn’t really count – then you’re paying for novelty and not much else).

That process can stop after any of the bullet items (including purchase). Nice-to-have is not likely to work for a large portion of this population – especially for those not technically inclined. There has to be real pain that you’re solving. And the consumer has to be aware of the pain.

For instance, in my earlier piece, I looked at water savings while doing laundry. That can be a real savings, but you’re going to address it only if you know specifically how much you’re spending on water for laundry; water bills don’t provide that detail. So someone else has to educate the consumer as to how much they’re really spending on water to wash clothes. And the numbers have to be credible – saying you’ll save $50/month won’t likely be taken seriously by someone with a $40 water bill, even if the (totally made up by me) $50 number is correct on average.

That’s just one simple example of the kind of work that needs to be done to motivate the value of CIoT technology to consumers – either that, or you need to re-assess whether, as a provider, you’re truly providing value. (As I’ve mentioned ad nauseum, the prime beneficiaries too often turn out to be not the users, but the data collectors who sell or use the data.)

Bottom line: the CIoT is still sputtering, looking for a compelling raison d’être – especially if you restrict your gaze to devices and applications truly requiring smarts via the internet. And I haven’t seen anyone provide a convincing story as to why that’s about to change. The onus is on the industry to make that change.

More info:

IDC webcast (Will ask for registration)

What are you seeing with respect to consumer IoT adoption?